Every December, the same panic sets in. Auditors want everything by January 15th, IRS deadlines are closing in, and suddenly you're drowning in reconciliation requests while trying to package W-2s and 1099s. Meanwhile, your team is surfacing discrepancies from Q2 that nobody caught, and you're building evidence binders at 11 PM wondering what you've missed.

The real problem isn't the volume of work. Most companies treat year-end payroll close like a once-a-year fire drill instead of a process they actually own. The difference between smooth closes and January nightmares comes down to having clear reconciliation templates, exception handling procedures, and an evidence packaging system that actually holds up under scrutiny.

Building your year-end payroll close checklist from reconciliations up

Your year-end close starts with reconciliations, not forms. Most businesses get this backwards—they rush to generate W-2s and 1099s, then scramble when the numbers don't match. A proper reconciliation framework catches issues while you still have time to fix them.

Start with your wage reconciliation baseline. Pull your quarterly 941s and match them against payroll register totals for each quarter. The numbers rarely match perfectly on first pass. Common culprits include manual adjustments that bypassed payroll, voided checks that weren't properly backed out, and mid-year system conversions where data got mangled somewhere along the way.

-

Gross wages per payroll system

-

Adjustments and manual entries

-

Voided or reversed payments

-

Net reportable wages

For each variance, document the source, the correction method, and who verified it. This becomes critical evidence for auditors who will absolutely ask about that $847.32 difference from Q3.

Your tax withholding reconciliation needs the same treatment. Federal withholding, state withholding, FICA—each gets its own reconciliation schedule. Pay close attention to employees who maxed out Social Security withholding mid-year. These consistently create headaches because different systems handle the cutoff differently.

Exception scenarios that derail January (and their fixes)

The terminated employee who got paid three times after leaving. It happens more than it should. Someone processes the final check manually, the system runs another automatic payment, and now you've got an overpayment situation crossing into the new year.

Eliminate payroll errors and delays.

Payexly streamlines every payroll cycle ensuring accuracy and compliance.

- Automated payroll processing

- Real-time tax compliance

- Benefits & deductions management

No credit card required

Your remediation template needs to address:

-

Recovery method (ACH reversal vs. repayment agreement)

-

W-2 correction requirements

-

State reporting implications

-

Documentation for uncollectable amounts

The contractor-to-employee conversion mid-year creates another common mess. They received 1099 income for five months, then W-2 wages for seven months. Some companies try to clean this up by recharacterizing all payments as W-2 wages. Don't. The IRS has specific rules about worker classification timing, and retroactive reclassification without following proper procedures triggers penalties.

Issue both forms with clear documentation showing:

-

The conversion date and business rationale

-

Board or management approval

-

Communication to the worker

-

Proper withholding implementation from the conversion date forward

Stock compensation creates its own category of reconciliation problems. RSUs that vested in December but weren't processed until January payroll. Options exercised where the withholding calculation was wrong. ESPP purchases where the discount wasn't properly included in wages.

-

Maintain a separate tracking schedule outside payroll

-

Reconcile quarterly, not annually

-

Document the FMV determination method for each grant

-

Keep exercise notices and withholding elections together

Document every communication attempt. If the employee doesn't respond, you'll need evidence showing good-faith recovery efforts before writing off the overpayment as additional income.

Packaging evidence that auditors actually want

Auditors don't want every payroll register from the entire year dumped into a shared folder. They want specific evidence packages that tell the story of your payroll controls and accuracy.

Structure your evidence binder with clear sections:

Section 1: Reconciliation Support

-

Quarterly 941 reconciliations

-

State withholding reconciliations

-

Year-end W-2/W-3 reconciliation

-

1099/1096 reconciliation

Section 2: Exception Documentation

-

List of all manual adjustments with approval evidence

-

Voided payment register with explanations

-

Employee status changes (especially contractor conversions)

-

Correction documentation for any amended returns

Section 3: Control Evidence

-

Payroll change reports for each pay period

-

New hire I-9 and W-4 compliance sampling

-

Termination checklist completion for departed employees

-

Tax deposit confirmations

Section 4: Special Situations

-

Multi-state employee allocation worksheets

-

Expatriate tax equalization calculations

-

Executive compensation limitation testing

-

Related retroactive pay corrections documentation

Pro-tip: Build the binder throughout December as you complete each reconciliation to avoid last-minute scrambling.

Don't wait until January to compile this. Build the binder throughout December as you complete each reconciliation. It prevents the last-minute scramble and means nothing slips through when you're tired and working against a deadline.

The W-2 and 1099 production line that actually works

Most companies treat form production as a technology problem—they assume their payroll system will just generate accurate forms. It won't. Your payroll system only knows what you've told it, and there's a good chance you've been feeding it incomplete information all year.

Before you even think about printing forms, run your validation checks. Pull every employee who had address changes during the year and verify the current address matches what's in the system. Check every employee with multiple state withholdings to confirm proper allocation. Review anyone with taxable fringe benefits to make sure imputation was handled correctly.

Your pre-filing validation process should catch:

-

Negative wage amounts (usually indicates over-corrections)

-

Missing SSNs or mismatched names

-

State wages exceeding federal wages

-

Zero federal withholding on high earners

For 1099s, the complexity multiplies. You're dealing with vendors who may have changed entity structures, incorrect TINs, and the perennial question of whether something is even reportable. Build a decision tree for borderline cases:

| Payment Type | Under $600 | Over $600 | Special Rules |

|---|---|---|---|

| Professional services | No 1099 | 1099-NEC | None |

| Rent | No 1099 | 1099-MISC Box 1 | None |

| Legal services | 1099-NEC | 1099-NEC | Required regardless of amount |

| Medical payments | No 1099 | 1099-MISC Box 6 | Special healthcare rules |

Document your decision process for edge cases. When an auditor asks why you didn't issue a 1099 to a consultant who received $587, you need evidence showing consistent application of reporting thresholds—not a shrug.

Creating reusable remediation templates

Stop rebuilding the same process every time you hit an exception. Build templates your team can execute without needing you in the room.

Template 1: Overpayment Recovery

-

Initial discovery documentation

-

Employee notification letter

-

Repayment agreement terms

-

Accounting entries for recovery or write-off

-

Tax form correction instructions

Template 2: Missing Tax Documentation

-

W-9 request letter (first, second, final notice)

-

Backup withholding implementation checklist

-

B-notice response procedure

-

TIN matching failure resolution

Template 3: Multi-state Allocation Correction

-

Workday analysis spreadsheet

-

State withholding recalculation

-

Amendment filing checklist

-

Employee communication template

Each template should include specific deadlines, escalation points, and decision criteria. Your overpayment recovery template might specify: attempt ACH reversal within 5 days, send written notice by day 7, escalate to legal if there's no response by day 30. The point is that your team shouldn't have to think through the logic every time—it should already be mapped out.

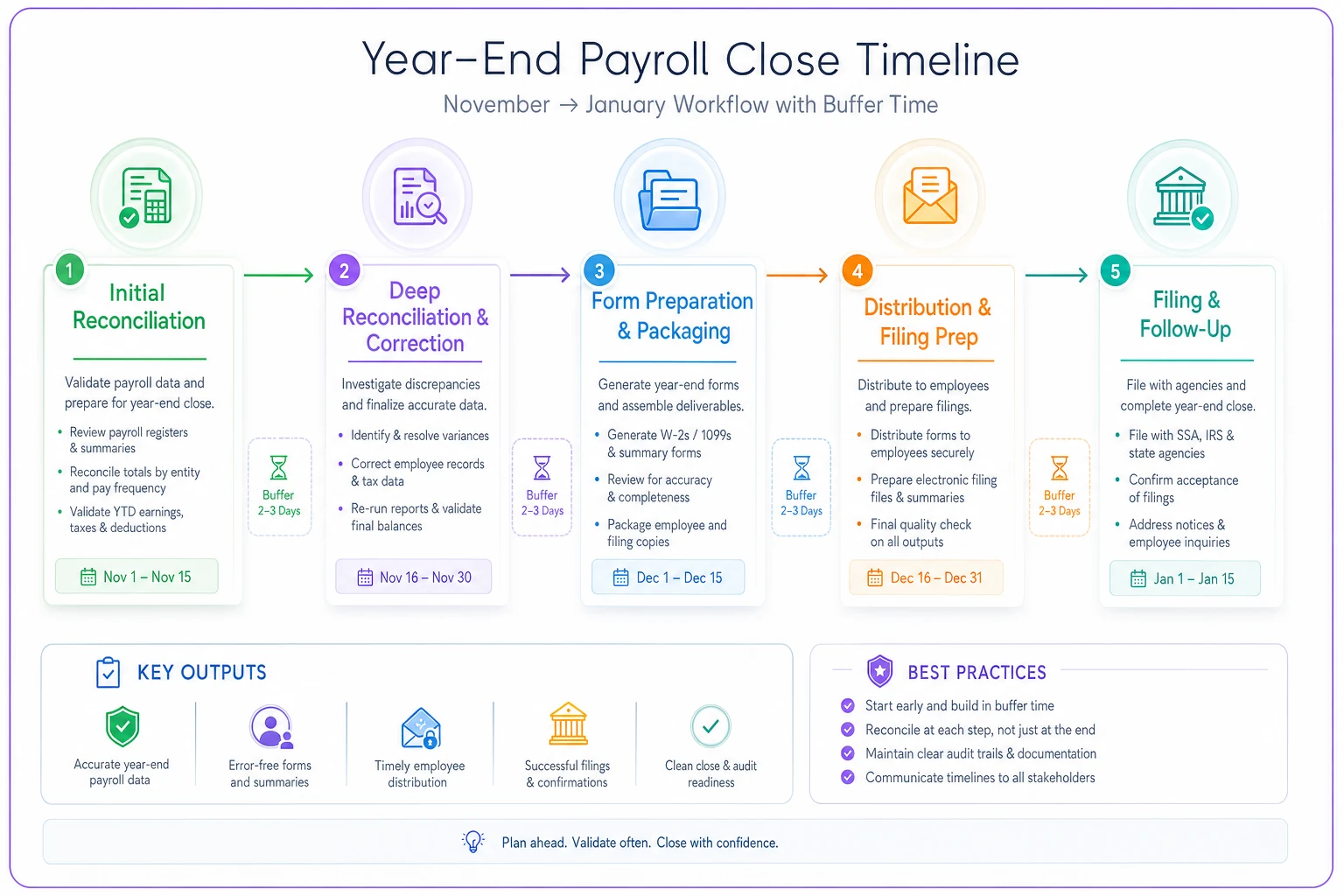

The timeline that keeps you out of crisis mode

December 1st isn't the start of year-end close—it's the deadline for having your reconciliation framework operational. Work backwards from your critical dates:

-

November 15–30 Initial reconciliation and exception identification - Run preliminary wage reconciliations - Identify major discrepancies - Start contractor/vendor verification

-

December 1–15 Deep reconciliation and correction - Complete all wage and tax reconciliations - Process necessary corrections in December payroll - Verify all employee addresses and SSNs

-

December 16–31 Form preparation and packaging - Generate draft W-2s and 1099s - Final validation checks - Compile audit evidence binder

-

January 1–15 Distribution and filing prep - Final form production - Employee distribution (electronic or mail) - Prepare federal and state filing packages

-

January 16–31 Filing and follow-up - Submit all required filings - Handle employee inquiries - Address any last-minute corrections

A simple visual of this timeline helps teams see the cadence and buffers.

This timeline assumes things go reasonably well. Build in buffer for the inevitable surprises—because there are always surprises.

The operational reality of year-end close

A mid-sized professional services firm discovered during their December reconciliation that their payroll service had been calculating state withholding incorrectly for remote employees all year. Roughly $45,000 in under-withheld taxes spread across 23 employees in 6 states.

The remediation required:

-

Amended quarterly returns for each affected state

-

Employee notifications about potential tax liability

-

Negotiation with states about penalty waivers

-

Additional withholding from December bonuses to partially offset

-

Detailed documentation for their auditors

They made it through because they found it December 10th, not January 10th. Their reconciliation process gave them three weeks to address it before W-2s went out. Three weeks is the difference between fixable and just expensive.

That situation illustrates why operational rigor matters more than having a perfect system. Your payroll platform might have solid automation and clean dashboards, but if you're not reconciling systematically, you won't know what's wrong until it's too late to fix it cleanly.

Making the evidence package auditor-friendly

Auditors have specific testing requirements they need to satisfy. Structure your evidence to map directly to common audit assertions:

Completeness Testing Evidence

-

Payroll register to G/L reconciliation

-

New hire listing to I-9 file comparison

-

Termination report to final payment verification

Accuracy Testing Evidence

-

Sample of gross-to-net calculations

-

Withholding rate verification

-

Benefits deduction authorization forms

Cutoff Testing Evidence

-

December and January payroll accruals

-

Final pay calculations for December terminations

-

Bonus accruals and subsequent payment

Include a cover sheet for each section explaining your methodology. Auditors appreciate context—knowing how you selected samples, why certain reconciling items exist, and what controls are in place saves everyone time and keeps the audit moving. A well-organized binder also signals that your team actually understands the process, which matters more than most people realize.

Building next year's foundation

Year-end close exposes every weakness in your payroll process. The manual workarounds, the Excel reconciliations held together with nested formulas, the corrections that take days to document properly.

Modern AI-powered operational software handles much of this more systematically—continuous reconciliation instead of year-end surprises, automatic exception flagging, centralized documentation instead of scattered spreadsheets. But even solid platforms require proper configuration and consistent execution. The tooling only works as well as the habits behind it.

The companies that cruise through year-end close treat it as a routine process rather than an annual emergency. They reconcile quarterly, maintain running exception logs, and keep documentation current throughout the year. An hour of cleanup in July genuinely does save a weekend in January.

The bottom line on year-end close

Your year-end payroll close checklist isn't just about compliance—it's about operational control. Every reconciliation you complete, every exception you document, every piece of evidence you organize properly reduces your risk and makes next year easier.

Start with solid reconciliation templates. Build exception handling procedures that actually work. Package evidence the way auditors expect to see it. Most importantly, treat year-end close as the result of good processes run consistently—not a heroic push to fix a year's worth of problems in three weeks. The businesses that handle this well don't have perfect systems or unlimited staff. They have clear processes, decent documentation habits, and the discipline to actually follow through.

Start with solid reconciliation templates. Build exception handling procedures that actually work. Package evidence the way auditors expect to see it. Most importantly, treat year-end close as the result of good processes run consistently—not a heroic push to fix a year's worth of problems in three weeks. The businesses that handle this well don't have perfect systems or unlimited staff. They have clear processes, decent documentation habits, and the discipline to actually follow through.

Ready to simplify your payroll operations?

Join 2,000+ businesses using Payexly to reduce payroll overhead, ensure compliance, and enhance employee satisfaction.