Three weeks ago, a controller at a 400-person manufacturing company discovered their overtime calculations had been wrong for six months. Not wildly off—just using 1.25x instead of 1.5x for Sunday shifts. The problem touched 47 employees across four departments. Total underpayment: roughly $82,000.

The fix seemed simple until they started unwinding the tax implications. Some employees had already maxed out their 401(k) contributions. Others had hit Social Security wage limits. A few had left the company. And Q3 941 forms were already filed.

That's where retroactive pay corrections get genuinely messy. You're not just cutting a check—you're recalculating taxes across multiple periods, amending filings, and potentially triggering penalties while trying to keep employees from panicking about their W-2s.

The detection problem nobody talks about

Most companies discover retroactive pay issues through accidents. An employee mentions their pay seems off. Someone catches a discrepancy during year-end reconciliation. A new HR person questions an old policy.

The real operational challenge isn't fixing the error—it's knowing it exists.

A logistics company with 220 drivers went 14 months paying incorrect mileage rates after a rate table update got partially applied in their payroll system. The error only surfaced when they switched payroll providers and ran parallel testing. By then, they owed $127,000 in back wages plus interest.

Manual detection relies on someone noticing something feels wrong. But when your payroll coordinator is processing 400+ employees biweekly, subtle errors slip through. A missing shift differential here. An incorrect commission calculation there. These compound over months until you're staring down a significant correction.

Companies that catch errors quickly usually have specific validation checkpoints built into their workflow. They compare period-over-period variances. They audit random samples of complex pay calculations. They track exception reports for unusual patterns.

Even with decent controls, certain errors hide well—incorrect tax withholding rates, misclassified employees, outdated benefit deductions. These don't trigger obvious red flags until someone actually digs.

Breaking down correction scenarios

Scenario 1: Same tax year, unfiled quarter

Eliminate payroll errors and delays.

Payexly streamlines every payroll cycle ensuring accuracy and compliance.

- Automated payroll processing

- Real-time tax compliance

- Benefits & deductions management

No credit card required

Best-case scenario. You discover and correct the error before filing quarterly returns.

Say you find in early October that September's commission calculations were wrong. You haven't filed Q3 941 yet. Calculate the gross pay difference for each affected employee, run it through your standard tax calculation engine to determine additional withholdings, and process corrections in your next regular payroll run as supplemental wages.

The journal entry is straightforward:

Commission Expense $24,500 Accrued Payroll $24,500 (To record additional commission owed) Accrued Payroll $24,500 Cash $17,885 Federal Income Tax Payable $4,900 FICA Tax Payable $1,715 (To record payment and withholdings)

Your Q3 941 includes the corrected totals. No amendments needed. Employees get accurate W-2s. The only real complexity is explaining the adjustment on pay stubs.

Scenario 2: Same tax year, filed quarter

Now it gets more complicated. You've already filed your 941 for Q2, but in Q3 you discover Q2 errors.

A retail chain with 180 employees discovered in August they'd been calculating overtime incorrectly since April. Q2 941 was already filed. They owed $43,000 in additional wages.

The correction workflow changes. First, decide whether to amend Q2 or adjust Q3. For errors under $25,000, many companies adjust the current quarter. Above that threshold, amendments usually make more sense for audit trail purposes.

If adjusting in Q3:

-

Process retroactive payments as supplemental wages

-

Add corrections to Q3 941 wages

-

Document thoroughly for potential IRS questions

-

Adjust your quarterly reconciliation worksheets

The journal entries get more involved:

Wage Expense - Prior Period $43,000 Wages Payable $43,000 (To record prior period adjustment) Wages Payable $43,000 Cash $31,390 Federal Tax Payable $8,600 FICA Payable $3,010 (To record retro payment) Payroll Tax Expense $3,010 FICA Payable $3,010 (To record employer portion)

If amending Q2:

-

File Form 941-X with detailed explanations

-

Pay any additional deposits owed

-

Calculate interest on late deposits

-

Update your records to reflect amended figures

Scenario 3: Prior tax year corrections

This is where controllers lose sleep.

A healthcare staffing firm discovered in March they'd misclassified 23 nurses as exempt throughout the previous year. Total overtime owed: $186,000. W-2s were already issued. Some nurses had already filed their personal tax returns.

Phase 1: Calculate corrections

-

Pull timecards for the entire prior year

-

Apply correct overtime rates

-

Calculate taxes using prior year rates

-

Determine interest owed on late payments

Phase 2: Issue Form W-2c

-

Prepare corrected W-2s for all affected employees

-

Include detailed explanations

-

Submit Copy A to SSA

-

Distribute to employees with clear instructions

Phase 3: Amend employer filings

-

File 941-X for each affected quarter

-

Calculate and pay failure-to-deposit penalties

-

Submit interest payments

-

Update state quarterly reports

The journal entries span multiple periods:

Prior Period Adjustment - Wages $186,000 Wages Payable $186,000 Wages Payable $186,000 Interest Expense $4,200 Cash $139,500 Federal Tax Payable $37,200 FICA Payable $13,500 (Including interest on late deposits)

Scenario 4: Multi-state complications

When corrections cross state lines, the complexity multiplies fast.

A tech company with remote employees across 12 states discovered they'd been withholding California state tax for an employee who'd moved to Texas eight months earlier. Meanwhile, they hadn't withheld Texas unemployment insurance.

Each state has different amendment rules. California wants amended DE-9 forms. Texas requires corrected C-3 quarterly reports. Some states charge penalties for late corrections. Others have voluntary disclosure programs with reduced penalties.

The operational workflow requires state-by-state analysis:

-

Which states allow adjustments in the current quarter?

-

Which require formal amendments?

-

What are the penalty structures?

-

Are voluntary disclosure agreements available?

This section ends with the operational considerations for multi-state corrections.

Employee communication templates that actually work

Generic "we made an error" emails destroy trust fast. Employees need specific information, delivered clearly.

For current employees receiving back pay:

Subject: Payroll Correction - Additional Payment Coming [Date] Hi [Name], During a recent payroll audit, we identified an error in how your [specific pay element] was calculated from [start date] to [end date]. You were underpaid by $[amount] over this period.

What happened: [Specific, brief explanation]

Your correction payment:

-

Gross additional pay

$[amount]

-

Federal tax withheld

$[amount]

-

State tax withheld

$[amount]

-

FICA withheld

$[amount]

-

Net payment to you

$[amount]

This will appear on your [date] paycheck as "Retro Pay Adjustment."

Tax implications: This correction will be included in your 2024 W-2. No action needed from you.

Questions? Reply to this email or contact [specific person] at [contact].

[Signature]

For employees who've terminated:

Subject: Important Payroll Correction - Payment Due to You [Name], We've identified a payroll error affecting your employment period with [Company]. You're owed additional wages of $[amount] for work performed between [dates].

Next steps:

-

Verify your current mailing address by replying to this email

-

We'll mail your check within 5 business days

-

You'll receive an amended W-2 by [date]

Important: If you've already filed your [year] taxes, you may need to file an amended return. The amended W-2 will include instructions.

Please respond within 10 business days to confirm your address.

[Signature]

For errors requiring employee repayment:

Never surprise an employee with a deduction. This one needs careful handling.

Subject: Important - Payroll Overpayment Discussion Needed [Name], We need to discuss a payroll error that resulted in an overpayment. You were paid $[amount] more than owed due to [specific reason].

Your options:

-

Single repayment

-

Payment plan over [X] pay periods

-

Other arrangement that works for you

Please contact me by [date] so we can find a solution that works for both of us. We understand this was our error and want to resolve it fairly.

[Signature]

IRS penalties and interest calculations

Failure to deposit penalties:

| Days Late | Penalty Rate |

|---|---|

| 1–5 days | 2% |

| 6–15 days | 5% |

| After 15 days | 10% |

| After IRS notice | 15% |

A construction company owing $67,000 in retroactive wages discovered the error 45 days after their Q2 941 due date. Their penalty calculation:

-

Additional employment tax owed

$9,500

-

Days late

45

-

Penalty rate

10%

-

Penalty amount

$950

Plus interest at current IRS rates

941-X amendment penalties:

Generally no penalties if you amend before an IRS notice. But interest accrues from the original due date regardless. The calculation gets layered with multiple periods—Q1 corrections run from April 30, Q2 from July 31, each quarter calculated separately. Current IRS interest rate sits at 8% annually, though it changes quarterly.

Building systematic detection workflows

The companies that minimize corrections don't just hope someone catches something. They build specific checkpoints into the process and assign clear ownership.

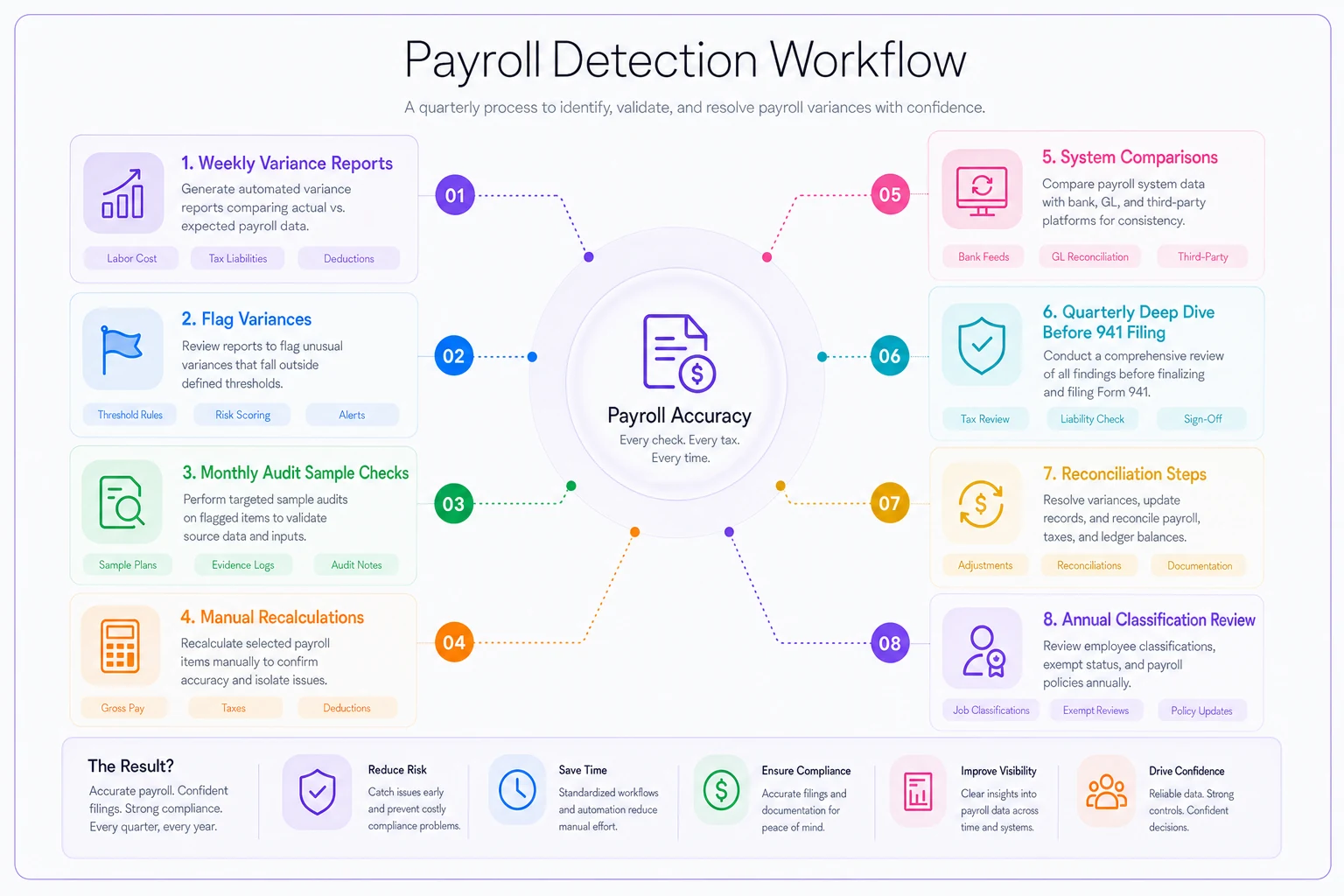

The diagram below shows how a typical quarterly detection cycle flows from weekly variance checks through the final pre-filing audit:

[Weekly Variance Report] ↓ [Flag variances >10% for review] ↓ [Monthly Audit Sample - 10 random employees] ↓ [Manual recalc: OT, commissions, differentials, withholdings] ↓ [Compare to system calculations] ↓ [Quarterly Deep Dive before 941 filing] ↓ [Reconcile register → GL → deposits → manual adjustments] ↓ [Annual Classification Review] ↓ [Exempt status, state jurisdictions, contractor classifications, tax tables]

Diagram shows a typical quarterly detection cycle and the checkpoints that help catch issues early.

Weekly variance reports compare the current period to the previous week, same week last month, and same week last year. Anything over 10% gets flagged for review.

Monthly audit samples pull around 10 random employees and manually recalculate overtime, commissions, shift differentials, and tax withholdings, then compare those numbers to what the system produced.

Quarterly deep dives happen before filing each 941—reconciling the payroll register to the general ledger, verifying tax deposits match obligations, reviewing final pay accuracy for terminated employees, and auditing manual adjustments.

Annual classification reviews cover exempt vs. non-exempt status, state tax jurisdictions, independent contractor classifications, and updated tax tables.

The goal isn't perfection. It's catching errors while they're still manageable.

System controls that prevent corrections

Lock prior periods after processing. Nobody should be modifying last month's payroll without an approval workflow. A marketing agency learned this the hard way after their payroll clerk "fixed" six months of errors directly in the system and created a reconciliation mess that took weeks to unwind.

Require dual approval for rate changes. When someone updates an hourly rate or salary, a second person verifies it before the next payroll run. Catches typos and miscommunications before they compound.

Lock prior periods and require dual approvals for rate or tax-table changes to prevent retroactive fixes that create complex reconciliations.

Automate tax table updates. Manual tax table maintenance causes a surprising number of errors. Systems that automatically pull updated federal, state, and local rates take that specific risk off the table entirely.

Build calculation transparency into pay stubs. When employees can see how their pay was calculated—hours × rate = gross pay—they catch errors faster than most internal audits will.

Force periodic master data reviews. Every quarter, have department managers verify their team's pay rates, classifications, and deductions. This distributed review catches changes that never got properly communicated to payroll in the first place.

The real cost of corrections

Beyond the actual wages and penalties, retroactive pay corrections carry hidden costs that don't show up on the initial damage estimate.

Employee relations take a hit immediately. Even when you're paying them more money, employees start wondering what else you've miscalculated. They scrutinize every pay stub going forward. They question their benefits calculations. Trust erodes in ways that are genuinely hard to rebuild.

Administrative burden multiplies with complexity. That $82,000 correction mentioned earlier? The company spent roughly 120 hours across payroll, HR, and finance unwinding it. Between amended filings, employee communications, and reconciliation updates, the soft cost exceeded $15,000.

Audit risk increases with amendments. File multiple 941-X forms and you've flagged yourself for potential review. The IRS may look at other periods, other tax types, other compliance areas. One correction can invite broader scrutiny than you bargained for.

Cash flow impacts hit at the worst times. You budget for normal payroll, not surprise corrections. A mid-size company might absorb a $20,000 correction without much disruption, but $200,000 affects operations. Add penalties and interest, and you're potentially pulling from budgets that were already committed elsewhere.

Moving toward prevention-first operations

The companies handling payroll best don't rely on catching errors after the fact. They prevent them through systematic workflows and clear ownership of each calculation type.

They document calculation logic explicitly. Not just "calculate overtime" but "multiply hours over 40 by 1.5x base rate, excluding commissions and bonuses from the base rate calculation." Specific enough that a new hire could follow it correctly on day one.

They test changes before they go live. One distribution company tests every commission structure change against ten real previous periods before implementation. Takes an extra day. Has saved them from at least three significant corrections over the past couple of years.

They maintain clear audit trails. Every change, override, and adjustment gets logged with who, what, when, and why. When questions come up months later, the documentation is already there.

Mostly, they treat payroll as an operational function rather than just a compliance task. It connects to scheduling, time tracking, benefits administration, and financial reporting. When these systems share data effectively, errors decrease on their own—there are fewer handoffs where things can go wrong.

AI-powered operational platforms have made a real difference here for companies willing to invest in them. Automated variance detection and built-in audit workflows tend to surface issues weeks earlier than manual review would. But whether you're using sophisticated software or well-structured spreadsheets, the underlying principles don't change: detect early, correct completely, communicate clearly, and actually prevent recurrence rather than just patching the immediate problem.

Putting it all together

Retroactive pay corrections will happen. Even well-run companies occasionally discover errors. The difference is how quickly you detect them, how cleanly you correct them, and whether you build real prevention into your process or just fix the immediate issue and move on.

Build detection workflows that catch errors within the same quarter. Create correction processes that minimize employee confusion and IRS penalties. Develop controls that stop errors before they have time to compound.

The real goal isn't perfect payroll—it's resilient payroll operations that handle corrections without turning into a crisis. When your workflows account for both normal processing and the inevitable occasional error, retroactive pay becomes a manageable process rather than a quarterly panic.

The next time you discover a retroactive pay issue, you'll know which scenario you're in and which workflow to follow. More importantly, you'll have the templates and processes to handle it without the situation spiraling into something bigger than it needs to be.

Ready to simplify your payroll operations?

Join 2,000+ businesses using Payexly to reduce payroll overhead, ensure compliance, and enhance employee satisfaction.